How to Shelter Assets on the FAFSA

When families search for “how to shelter assets for FAFSA,” they’re usually trying to answer a few very practical questions:

- Will assets hurt financial aid?

- What assets count on the FAFSA?

- What assets don’t count?

- Are there legal ways to minimize the impact of assets before filing?

- What old FAFSA advice is no longer accurate?

Here’s the important framing: you can’t hide assets on the FAFSA. The FAFSA needs to be accurate, and intentionally false information can lead to serious penalties.

But you can understand how FAFSA assets work, which assets are excluded, and what legal planning decisions may matter before you file.

That’s what this guide is about: knowing the rules so you can avoid over-reporting, avoid common mistakes, and make informed decisions.

TL;DR: How assets affect the FAFSA

- Assets can affect financial aid, but they are only one part of the FAFSA calculation. Income usually has a bigger impact.

- The FAFSA may ask about assets like cash, checking and savings accounts, investments, certain real estate, businesses, farms, 529 plans, trusts, and cryptocurrency.

- Some assets do not count on the FAFSA, including your family’s primary home, retirement accounts, life insurance value, personal belongings, and ABLE accounts.

- Some families may qualify to skip asset reporting entirely, depending on income, tax filing details, Pell eligibility, or receipt of certain federal benefits.

- Who owns the asset matters. Student-owned assets are generally assessed more heavily than parent-owned assets.

- FAFSA looks at assets as a snapshot on the day you submit the form, so use current values and don’t report negative asset amounts.

- Legal FAFSA planning is about understanding the rules, avoiding over-reporting, and using accurate information,not hiding money.

- Watch out for common mistakes, like reporting excluded assets, including sibling 529 plans, relying on outdated business/farm rules, or assuming FAFSA and CSS Profile use the same asset rules.

Do assets affect financial aid?

Yes, assets can affect financial aid eligibility, but they’re only one part of the FAFSA calculation.

Income usually matters more, but FAFSA asset reporting still matters if you’re required to answer those questions. The FAFSA form may collect current information about cash, savings, checking accounts, investments, real estate, businesses, and farms as of the day the form is signed.

The key things to know:

- Some families may not have to report assets at all.

- Some assets count.

- Some assets are excluded.

- Student-owned assets and parent-owned assets can be treated differently.

- Timing matters because FAFSA looks at a snapshot of your finances.

So, yes: assets can matter. But the goal is not to “game” the FAFSA. The goal is to report the right assets correctly.

Start here: You might not have to report assets at all

Before you worry about moving money around, check whether you’re required to report assets in the first place.

Some FAFSA applicants are exempt from asset reporting. For example, asset information may not be used in the SAI formula for some applicants based on Pell eligibility, income level, tax filing details, or receipt of certain means-tested federal benefits.

You may qualify for an asset-reporting exemption if one of these applies:

- You qualify for an automatic zero or negative Student Aid Index (SAI).

- You’re a dependent student and your parents’ AGI is under the FAFSA threshold, with certain tax schedule limits.

- You’re an independent student and your AGI is under the FAFSA threshold, with similar tax schedule limits.

- Someone in your household received a means-tested federal benefit in the prior 24 months, such as SNAP, SSI, TANF, WIC, Medicaid, or federal housing assistance.

There are some exceptions, including special rules for certain dependent students whose parents do not live in the U.S. or a U.S. territory or do not file U.S. taxes.

Why this matters: if you qualify to skip asset reporting, your best “asset strategy” may simply be understanding that your assets won’t be used in the federal aid calculation.

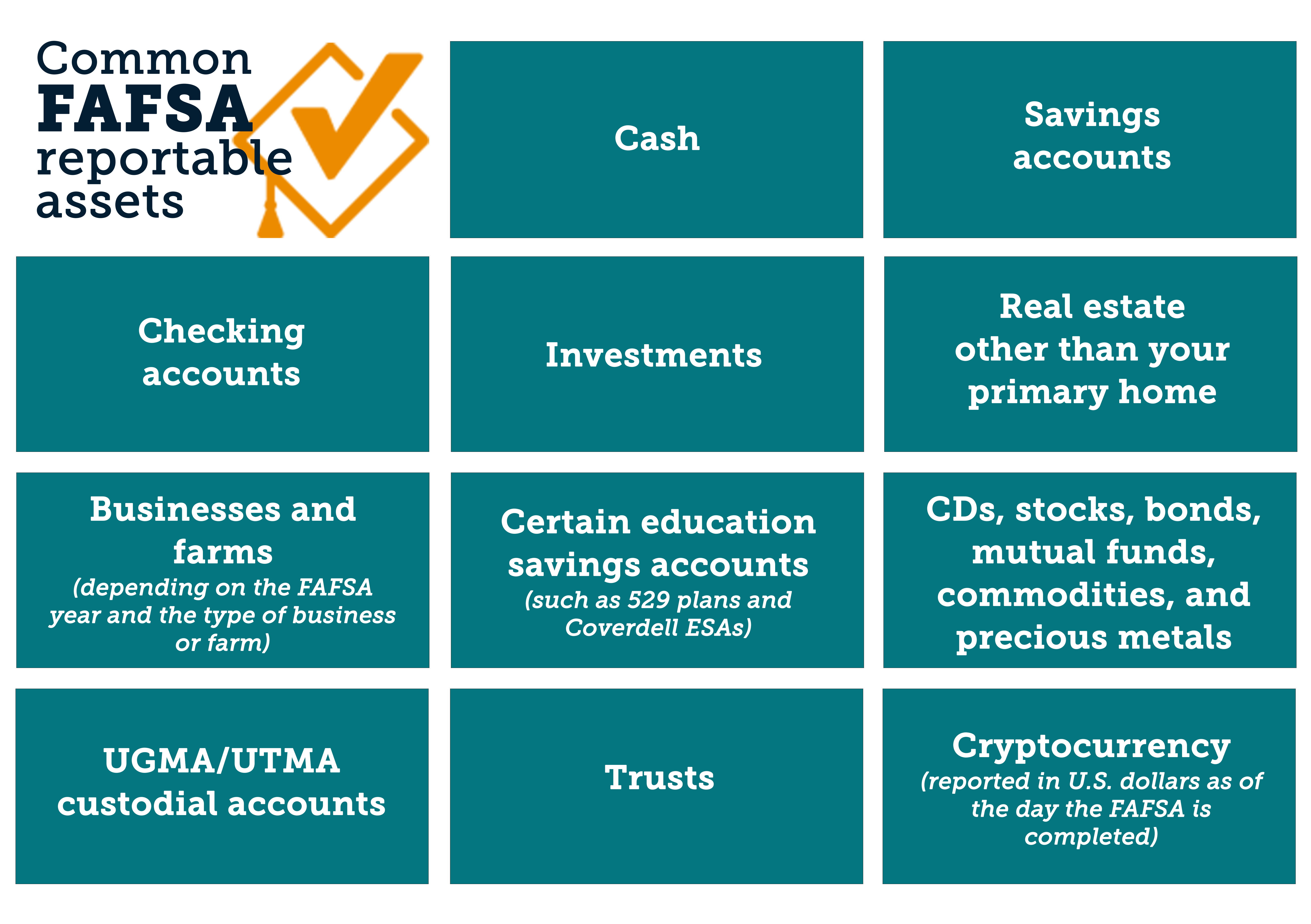

What assets count on the FAFSA?

If you are required to report assets, FAFSA generally asks for the current value of assets that are considered available for education expenses.

Common FAFSA-reportable assets include:

Federal Student Aid says families may need records for cash, checking, savings, investments, businesses, and farms when completing the FAFSA.

The practical takeaway: gather your numbers before you file, and make sure you’re reporting the value as of the day you submit the FAFSA.

What assets do not count on the FAFSA?

Not everything you own belongs on the FAFSA.

Excluded assets generally include:

For 2026–27, Federal Student Aid guidance says applicants should exclude family businesses with 100 or fewer full-time or full-time equivalent employees, farms where the family resides, and family-owned commercial fishing businesses and related expenses.

This is where a lot of families make mistakes. If something is excluded, don’t report it just because it feels financially important. FAFSA is asking for specific assets, not everything your family owns.

How FAFSA treats cash, investments, businesses, and home equity

Different asset types can be treated differently. Here’s what to know for each asset type:

Cash, savings, and checking accounts

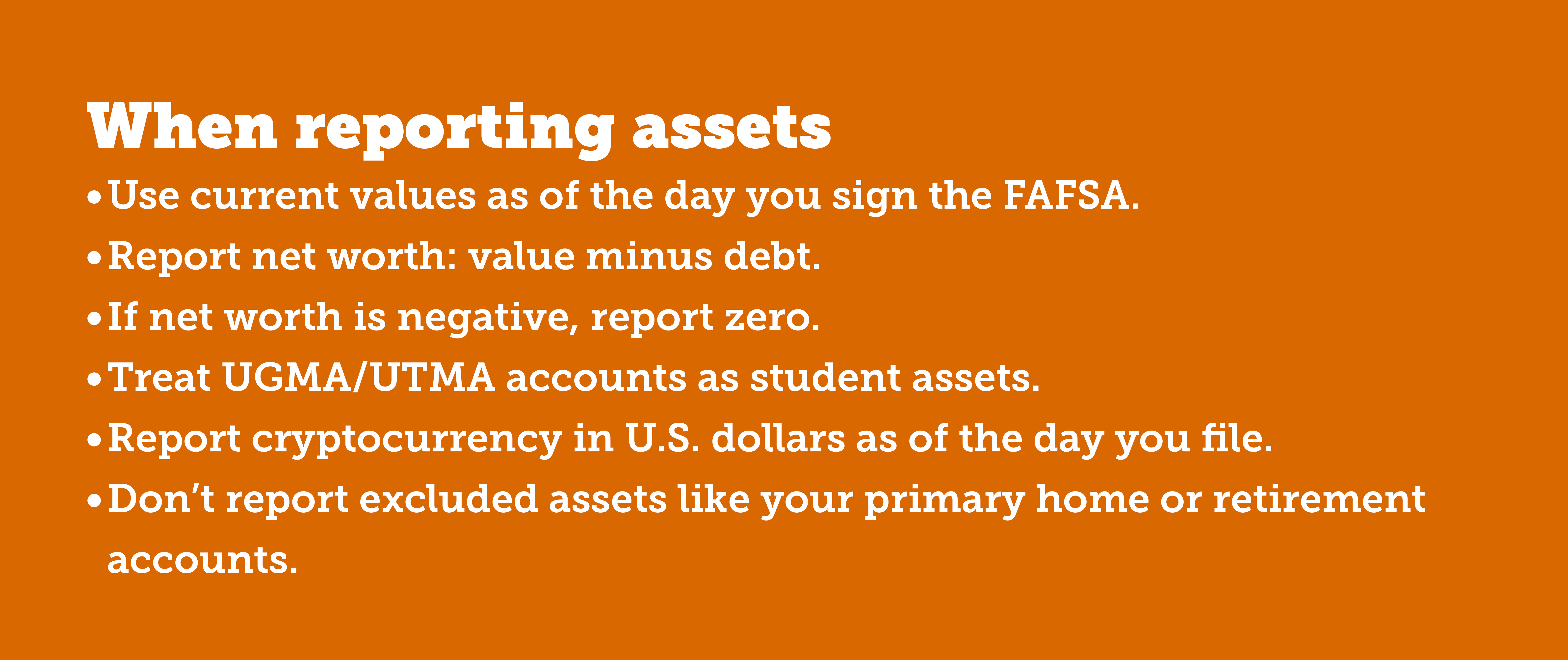

FAFSA looks at your current balances as of the day you submit the form.

That means timing matters. FAFSA is not asking what you had last year or what you expect to have later. It is asking what you have when you file.

If the balance is zero or negative, report zero. Don’t enter negative numbers.

Investments

For FAFSA, investments can include things like:

- Real estate other than your primary home

- Vacation homes

- Rental property

- Trusts

- Stocks and bonds

- Mutual funds

- Money market funds

- CDs

- Qualified education benefits, including 529 plans

You report the net worth of investments, which means the current market value minus debt owed against them. If debt exceeds value, report zero — not a negative number.

Student assets vs. parent assets

Who owns the asset matters.

For dependent students, parent assets and student assets are not treated the same way. In the 2026–27 SAI formula, parent assets are converted at 12%, while dependent student assets are converted at 20%. Independent students without dependents also use a 20% asset rate, while independent students with dependents use a 7% rate.

That’s why counselors often warn families to pay close attention to assets in the student’s name, especially custodial accounts.

Quick example: parent savings vs. UTMA

Situation: A family has $5,000 saved for college.

If that money is in a parent savings account, FAFSA treats it as a parent asset.

If it’s in a UTMA or UGMA custodial account, FAFSA treats it as the student’s asset because the student is the owner.

Why it matters:

- $5,000 as a parent asset could increase SAI by up to $600.

- $5,000 as a student asset could increase SAI by up to $1,000.

Same amount of money. Different FAFSA treatment.

529 plans and other education savings

FAFSA treats qualified education benefits as assets. That includes:

- 529 college savings plans

- Coverdell ESAs

- Refund value of 529 prepaid tuition plans

Here’s the part that trips people up: for a dependent student, a 529 plan is reported as a parent investment if the account is designated for that student. Accounts designated for other children in the family are not included.

Practical takeaway: if your family has multiple 529 plans, organize them by beneficiary before filing. Report only the account tied to the student whose FAFSA you’re completing.

Businesses and farms

This depends on which FAFSA year you’re filing.

For 2025–26, FAFSA guidance says applicants may be asked to report the net worth of businesses and farms, regardless of size, where the family lives, or number of employees. The family’s primary residence is still excluded, even if it is located on business or farm property.

For 2026–27, Federal Student Aid announced that the SAI asset calculation excludes:

- A family-owned business with 100 or fewer full-time or full-time equivalent employees

- Farms where the family resides

- A family-owned commercial fishing business and related expenses

Those should not be reported as FAFSA assets beginning with the 2026–27 award year.

Practical takeaway: check the rules for the FAFSA year you’re filing. This is an area where old advice can become outdated quickly.

Home equity

Your primary home is not reported as a FAFSA asset.

That’s true even if the home is part of a family farm or used in connection with a family business.

But other real estate, such as rental property, vacation homes, or income-producing property, may count as an investment.

Trusts, custodial accounts, and crypto

These are some of the most confusing FAFSA asset categories, so we’ll break these down separately:

Cryptocurrency

FAFSA treats virtual currency, such as Bitcoin, as an asset. You report its value in U.S. dollars as of the day the FAFSA is completed.

UGMA and UTMA accounts

UGMA and UTMA accounts count as the minor’s asset, not the parent’s asset, because the minor is the owner.

That can matter because student assets are generally assessed more heavily than parent assets.

Trust funds

Trust funds are generally treated as assets of the named beneficiary, even if access to the money is restricted.

The main exception: if a trust is restricted by court order, it may not need to be reported.

Contested assets

If ownership of an asset is being legally contested, it should not be reported. But if the dispute is resolved after the FAFSA is filed, the value cannot be updated for that FAFSA year.

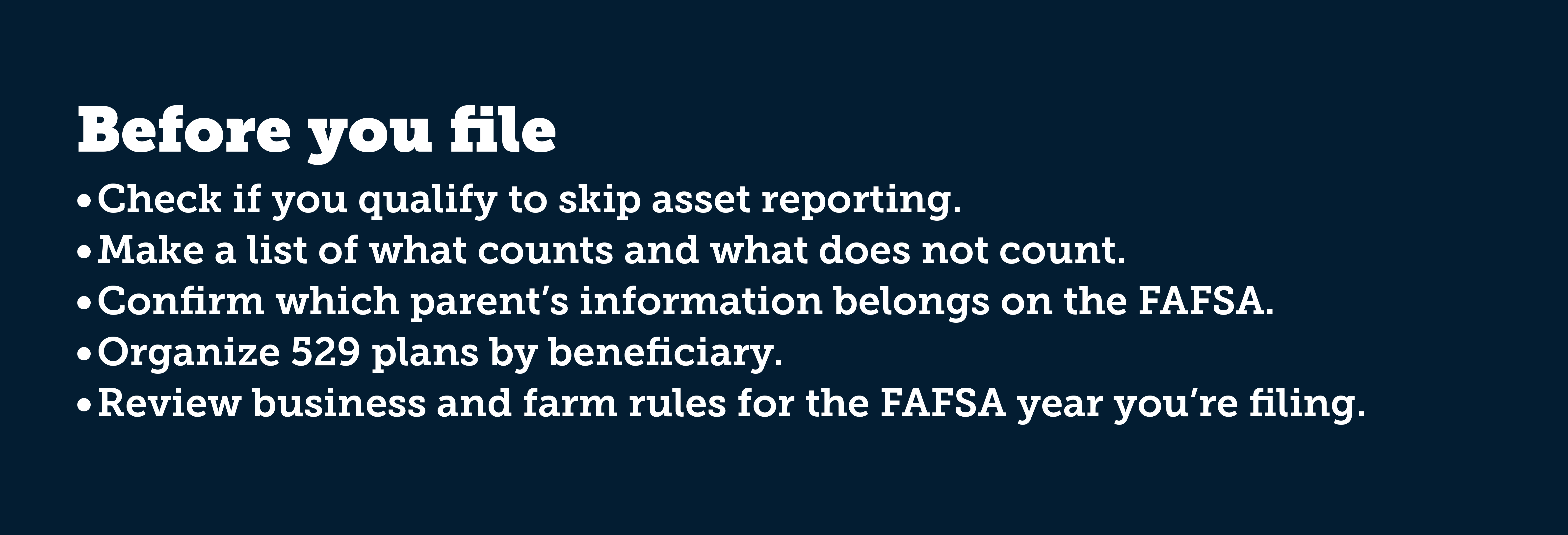

Legal ways families may plan ahead before filing

Families do want to maximize aid eligibility, and that’s a fair goal.

The safe way to do that is by understanding FAFSA rules before you file — not by hiding money or making last-minute moves that could create problems.

Here are legal, realistic planning steps that may help:

1. Check whether you’re exempt from asset reporting

This is the biggest one. If you qualify to skip asset reporting, complicated asset planning may not matter for the federal calculation.

2. Make a “counts vs. doesn’t count” list

Before filing, separate assets into two groups:

- Assets FAFSA asks you to report

- Assets FAFSA excludes

This helps prevent over-reporting.

3. Pay attention to ownership

Money in a student-owned account can be treated differently from money in a parent-owned account.

This matters most for custodial accounts, savings accounts, and education savings plans.

4. Organize 529 plans by beneficiary

If you have more than one child, don’t automatically total all 529 plans together. For a dependent student, only the 529 designated for that student is reported.

5. Use the correct FAFSA year rules

Business and farm reporting rules changed for 2026–27, so don’t rely on old articles or outdated advice.

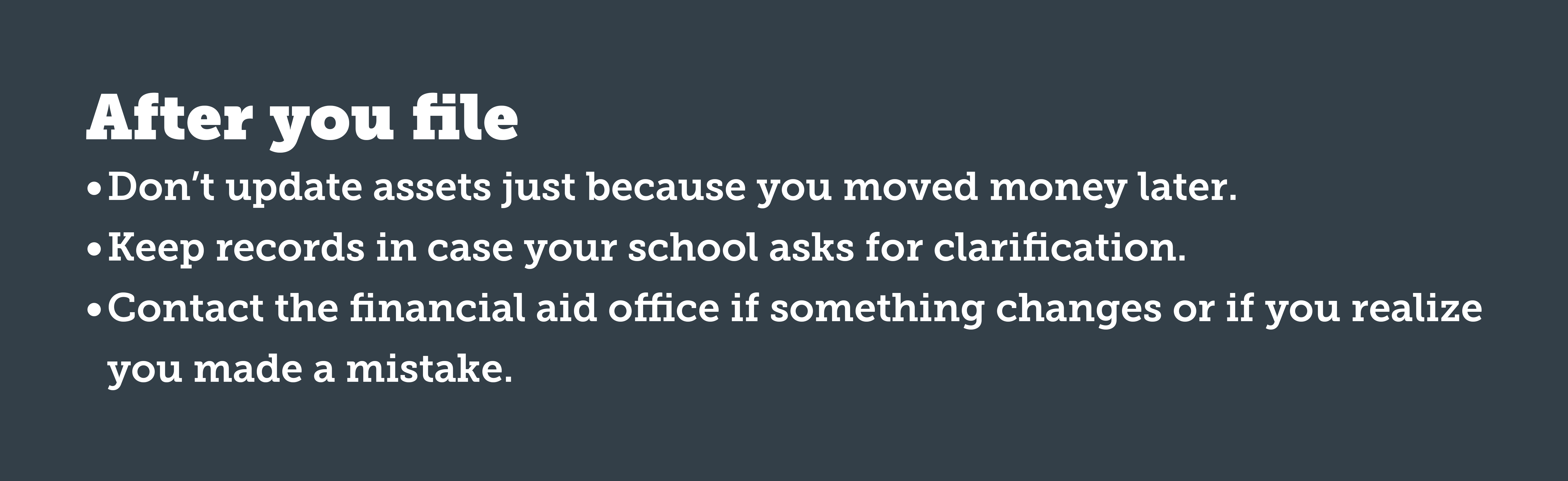

6. Don’t update assets just because you moved money after filing

FAFSA is a snapshot. In general, asset values are reported as of the day the FAFSA is signed and can only be updated in certain circumstances.

7. Ask for help if your situation is complicated

If you own a business, have trusts, have divorced or separated parents, or support dependents, it’s worth checking with the financial aid office or a trusted advisor before filing.

Common FAFSA asset mistakes and misunderstandings

A lot of FAFSA asset mistakes come from assumptions that sound reasonable but are wrong.

Mistake 1: Reporting excluded assets

Don’t report your primary home, personal possessions, retirement accounts, life insurance value, or ABLE accounts just because they feel like part of your financial picture.

FAFSA excludes them.

Mistake 2: Reporting negative asset values

If an investment’s debt is higher than its value, report zero. Negative numbers don’t lower your asset total.

Mistake 3: Reporting every 529 plan in the family

For a dependent student, report the 529 designated for that student. Accounts for siblings are not included.

Mistake 4: Treating all parent situations the same

If parents are divorced or separated, FAFSA does not automatically use the parent the student lives with most. It uses the parent who provided more financial support over the last 12 months. If support is truly equal, the parent with greater income and assets is used.

Mistake 5: Thinking taxes decide the FAFSA parent

FAFSA does not care who claims the student on taxes, who has primary custody on paper, or who feels like the “main” parent.

It cares about contributor rules and financial support.

Mistake 6: Forgetting about stepparents

If the parent who belongs on the FAFSA is married or remarried, the stepparent may also need to contribute financial information.

Mistake 7: Relying on old retirement-account advice

A lot of older FAFSA advice was written before FAFSA simplification. Some broad “untaxed income” categories are no longer part of federal need analysis, while certain self-employed retirement deductions may still matter depending on how they appear on tax returns.

Mistake 8: Assuming FAFSA and CSS Profile use the same rules

The CSS Profile is separate from the FAFSA. Some colleges use it to award institutional aid, and it may ask for more detailed financial information than the FAFSA.

For federal student aid, FAFSA is the main form. But for state aid, institutional scholarships, or college-based grants, schools may request additional information.

What these rules look like in practice

We know that was a lot. Let’s make it more concrete.

Scenario 1: Student savings vs. parent savings

A student has $5,000 saved for college.

If the money is in a parent savings account, it is treated as a parent asset.

If the money is in a UTMA or UGMA account, it is treated as a student asset.

Because FAFSA assesses student assets more heavily, the same $5,000 could have a bigger impact if it is in the student’s name.

Scenario 2: The sibling 529 mix-up

A family has three 529 plans, one for each child.

Common mistake: reporting the total value of all three.

What FAFSA wants: for a dependent student, report the 529 plan designated for that student. Do not include accounts designated for other children.

Scenario 3: Business owner filing for 2026–27

A family owns a small business with fewer than 100 full-time employees.

For 2026–27, that business may be excluded from FAFSA asset reporting.

For 2025–26, the reporting rule may be different.

Takeaway: always check the FAFSA year.

The safe FAFSA asset checklist

Looking for scholarships

If you're looking for scholarships you can actually apply for, create a free Appily account to explore our scholarship database. All scholarships are vetted, so you know they're real and safe to apply for. You can search by eligibility, interests, and graduation year. Just click the button to get started!

FAQ about reporting assets on the FAFSA

Will assets hurt financial aid?

They can, but assets are only one part of the FAFSA calculation. Income usually plays a larger role. The impact also depends on the type of asset and who owns it.

What assets count on the FAFSA?

Cash, savings, checking accounts, investments, certain real estate, education savings accounts, businesses, and farms may count, depending on your situation and FAFSA year.

What assets do not count on the FAFSA?

Your primary home, personal possessions, retirement accounts, life insurance value, and ABLE accounts are generally excluded. Some businesses and farms are also excluded beginning with 2026–27.

Can families legally reduce the impact of assets?

Yes, but the safest approach is understanding the rules, avoiding over-reporting, organizing assets correctly, and planning ahead. The goal is legal accuracy, not hiding money.

Does FAFSA count home equity?

No. FAFSA does not count the equity in your family’s primary residence.

Do 529 plans count on the FAFSA?

Yes, but the treatment depends on ownership and beneficiary. For a dependent student, a 529 designated for that student is generally reported as a parent asset.

Do retirement accounts count on the FAFSA?

Retirement account balances are generally not reported as FAFSA assets. However, some retirement-related tax items may still matter depending on how they appear on tax returns.

Does FAFSA count cryptocurrency?

Yes. Virtual currency is treated as an asset and should be reported in U.S. dollars as of the day the FAFSA is completed.

Which parent’s assets count if parents are divorced or separated?

FAFSA uses the parent who provided more financial support during the last 12 months. If support is exactly equal, the parent with greater income and assets is used.

Is the CSS Profile the same as FAFSA?

No. The CSS Profile is a separate form used by some colleges and scholarship programs for institutional aid. It may ask for more detailed financial information than the FAFSA.