How to Read a Financial Aid Award Letter

Congratulations are in order. You’ve received your college acceptance and financial aid award letters. Now you need to review and compare your offers and decide which school you'll attend.

Unfortunately, financial aid award letters can be confusing. What might look like a good deal on paper can end up being the option that costs you the most. For this reason, it's essential to understand financial aid award letters.

In this article, we'll explain how to interpret and compare financial aid offers so you can decide which offer is best. We also share some expert advice from our friend, Marie D. Johnson, Director of Student Financial Services at the University of Vermont. So let’s get started.

Click the image to watch!

What is a Financial Aid Award Letter?

Financial aid award letters outline a school’s offer of financial assistance in the form of grants, scholarships, loans, and work-study options. Colleges and universities use the information you provide on your FAFSA to determine how much financial aid you are eligible to receive.

When Will I Get My Financial Aid Award Letter?

You’ll first need to complete a school’s application requirements and fill out the Free Application for Federal Student Aid (FAFSA). From there, most schools send their financial aid offers out at about the same time they send their acceptance letters. That means you’ll likely get your financial aid award letter at the same time or within the same month as you get your acceptance letter. But each school is different, and when you apply matters too.

Understanding Your Financial Aid Award Letter

To start, you’ll want to pull out the most important parts of your award offer. We’ll highlight them now.

Cost of Attendance (COA): This is an estimate of what one full year of school will cost. It includes tuition, fees, room/board, books, transportation, and more. If this total sum is not listed on your financial aid award letter, check your school’s website or reach out to someone at the school. You absolutely need this number to understand your offer.

Scholarships & Grants: These types of financial aid need not be repaid. Grants are usually based on financial need, while scholarships can be based on merit, need, or other factors.

Federal Work Study: This type of financial aid allows students to work part-time on campus in exchange for money to help pay for their education.

Student Loans: These must be repaid with interest. Financial aid award letters will typically list the types of loans a student is eligible to receive, as well as the interest rates and repayment terms. Pay special attention to these details. They’re critical.

Carefully review the types and amounts of aid listed. Then, consider the terms and conditions of each type of aid. Remember, grants and scholarships are preferred to loans since you don't need to pay them back.

Once you understand what’s on the offer, subtract the total amount of free aid from the total cost of attendance to see how much you will need to pay out of pocket. This remaining amount is the net price of attending that school.

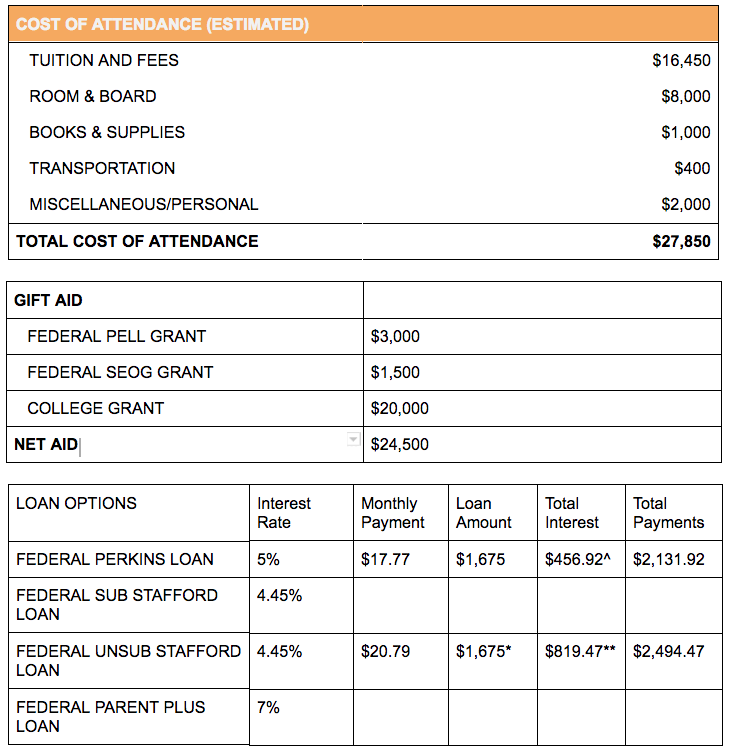

Sample Financial Aid Award Letter

If you're interested in seeing how a financial aid award might be broken out, here's an example.

You probably already figured everything out if you know what you’re looking at. The total estimated cost of attendance is $27,850. The financial aid offered is $24,500, which only leaves a difference of $3,350.

But remember, you get a new financial aid award each year. So hypothetically, you'd need to pay $3,350 each year or $13,400 for a four-year degree.

Tips for Navigating Student Loans in Your Aid Award

If you haven’t been offered enough scholarships or grants and need to take advantage of loans, you’ll want to leverage federal student loans first and foremost.

Federal student loans are less expensive. They typically have lower, fixed interest rates that the government sets. Alternatively, private student loans may have variable interest rates set by a bank or credit union. Also, federal student loans do not require collateral, while private student loans may require a co-signer or collateral to secure the loan.

For these reasons, you should always take advantage of federal student loans before any private loans. Better yet, look for private scholarships to access additional free money to pay for school.

Comparing Financial Aid Offers

Next, you have to compare your offers by isolating the net price for each school. Again, incorrectly comparing offers or not comparing them at all is a mistake that costs students money.

Marie D. Johnson, Director of Student Financial Services at the University of Vermont, explains, “It is important to understand how to compare aid offers to know the costs of various options. Sometimes people believe that because one school has a larger scholarship or aid offer than another, it automatically means the school is lower cost.” But that’s not the case at all.

Maria continued, “ To determine the bottom line cost after aid for each school, focus on laying out tuition, fees, housing, and food costs and then deduct only scholarship and grant offers for each school to compare them.”

If you add student loans to the total aid amount in the equation, you’re not getting an accurate estimate of out-of-pocket costs since you’ll have to pay back the loans plus interest. Free money always beats money you have to pay back. So keep that in mind as you compare offers.

“Another important thing to consider is what the tuition covers,” Maria told us. “Some schools charge per credit. Other schools provide a range of credits per semester which can help to contain costs as most programs require students to earn 15 credits per semester for a 4-year, 8-semester program.”

Financial Aid Comparison Worksheet

Now that we’ve explained how to compare offers, you can use a worksheet like this one to lay out your numbers and see how they stack up.

Common Mistakes When Reviewing Financial Aid Award Letters

People make several common mistakes when evaluating their financial aid award letters and deciding which school to attend. We’ll cover them now.

- Not understanding the terms and conditions of each type of aid

It's important to carefully review each type of financial aid listed on the award letter. Too often, students confuse loans with grants and scholarships and carry a significant debt upon graduation. Don’t do this.

- Not understanding the total cost of attendance

As we’ve explained, financial aid award letters typically list the total cost of attendance. This should include tuition, fees, room and board, and other expenses. Understanding this number is essential, as it’s the starting point for comparing offers and making a sound decision.

- Not comparing financial aid offers from multiple colleges

As our expert, Marie D. Johnson, shared, you should compare offers to see which gives you the most favorable outcome. You may still choose to attend a college that gives you less free aid money than another. But at least you’ll have the facts and make an informed choice.

- Not considering the long-term implications of taking on debt

If you are offered loans as part of your financial aid package, consider the long-term implications of taking on this debt. For example, be sure to understand the interest rates, if they’ll change or stay fixed throughout the life of the loan, when interest will begin to accrue, the repayment terms, and the potential impact taking on loans could have on your credit score and ability to borrow money in the future.

- Not appealing for additional aid

If you are not satisfied with a financial aid offer, you may be able to appeal to the college or university for additional aid. Conventional wisdom says you must have an excellent reason to appeal a disappointing financial aid award, such as a job loss, a death, a divorce, large medical bills, or other exceptional circumstances. But that's not always the case. Check out our article linked above to learn more.

Private Scholarships to Supplement Your Financial Aid Award

Now that you have an accurate understanding of how much it will cost you to attend college at your chosen school(s), you might want to pick up a little extra scholarship money.

Simply log in to your free Appily account to access an extensive and up-to-date list of scholarships. You can save those you’re interested in and come back to apply for them later. Just click the button now.