Do I Qualify for Student Loan Forgiveness?

New college graduates hear a lot about student loan discharge and cancellation and it's an appealing idea. After all, who wouldn't want permission to not pay back tens of thousands of dollars? But don't be fooled by promises of quick and easy loan discharge or cancellation; few grads actually qualify for these programs. Who can have their loans forgiven or canceled? You have a chance of qualifying, so here are a few ways to be considered.

You Work in Public Service

Educators who obtained a Direct Loan or Federal Family Education Loan (FFEL) after October 1, 1998, may qualify for loan forgiveness. You must have taught full-time at a low-income primary or secondary school (or educational service agency) for five consecutive years. Under the Teacher Loan Forgiveness program, you could have up to $17,500 of your loans forgiven.

The Public Service Loan Forgiveness program means working in public service can lead to student loan forgiveness for direct loan borrowers. To qualify, you must have made 120 on-time loan payments and you cannot be in default on the remaining balance.

Like public service loan forgiveness, Perkins Loan cancellation and discharge allows people who are employed in certain jobs or fields to have a portion of their loan canceled for the years they work in these careers. Nurses, military members, law enforcement professionals and Peace Corps volunteers are examples of the types of individuals who can benefit.

You're Incapable of Paying Back the Loan

If you've been rendered totally and permanently disabled (TPD), you may qualify for a student loan discharge. You'll need to provide information about your disability to the Department of Education, which will then determine if the TPD discharge applies to your situation. The Department of Education has information on how what type of information you can submit for a TPD discharge.

Few students will qualify for discharge in bankruptcy. If you've filed for Chapter 7 or Chapter 13 bankruptcy, you must prove to the court that repaying your student loan would cause undue hardship. You'll need to prove that paying the loan would hinder your ability to maintain a minimal standard of living and this hardship will continue for an extended period. You must also prove that you made efforts to repay the loan before filing for bankruptcy (typically for a period of at least five years).

Your School Closed or Defrauded Students

If your school closed while you were a student or within 120 days after you withdrew, 100% of your direct loans, Perkins Loans and FFEL may be discharged. Note that this does not apply to students who withdrew more than 120 days before the school closed, completed all coursework for the program they were enrolled in or students who are completing a similar program at another institution. Students who think their school committed fraud, misrepresented its services or violated the law may also qualify for discharge.

Other Instances of Loan Forgiveness or Discharge

If your loan was falsely certified because you were a victim of identity theft or if your school signed your name on the application or promissory note without your authorization, you may qualify for False Certification of Student Eligibility or Unauthorized Payment Discharge. You can also have your loan discharged under this program if your school certified your eligibility, despite your inability to work because of a criminal record, health condition or other factors.

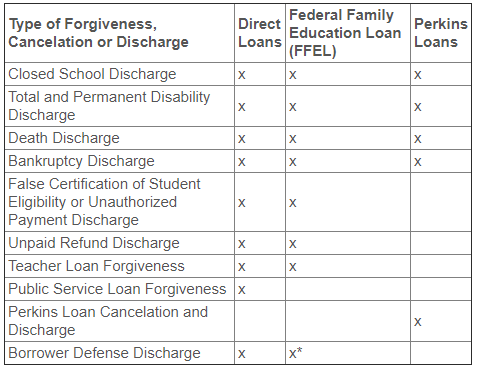

Another type of discharge is an unpaid refund discharge. If a student withdraws from a college or university and the school does not repay the Department of Education or designated lender the money owed, he or she may qualify for this discharge. Also, if a student borrower dies, their loans will be discharged with a Parent PLUS Loan. Here's a handy chart from the Department of Education that will help you better understand which loans qualify under different programs.

*Borrowers may submit defense claims with regard to FFEL Program loans against the holder of the loan only under the circumstances described in 34 CFR 682.209(g).